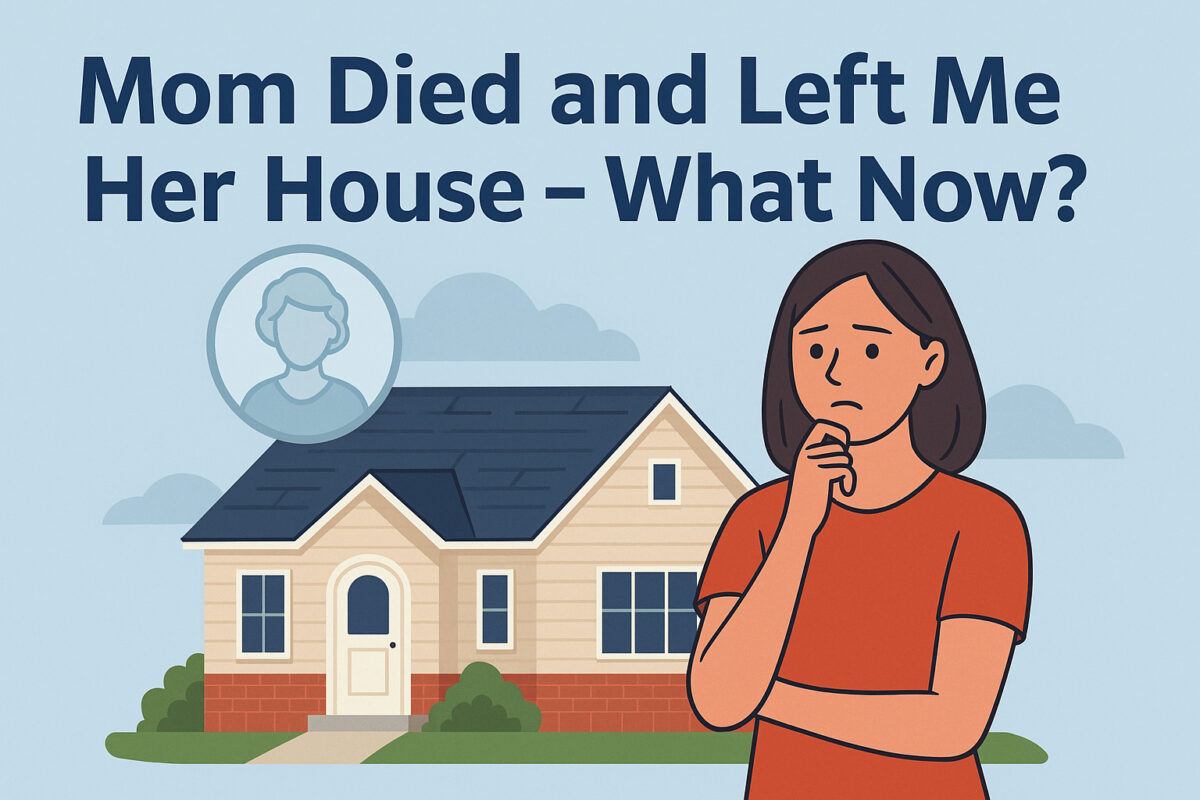

Your mom is gone, and you’re sitting in her empty house in Lakewood, looking at 40 years of memories. The funeral was last week. People keep asking “what are you going to do with the house?” and you honestly have no idea.

You’re grieving, overwhelmed, and now you’re supposed to make major financial decisions about a property you never expected to own. Mom’s coffee cup is still in the sink, but the insurance company is calling about payments.

This isn’t what you signed up for. You wanted to inherit your mom’s love and wisdom, not a 1970s ranch house with a leaky basement and a yard you don’t know how to maintain.

It’s okay to feel lost. You’re not alone, and there’s no “right” way to handle this.

The Burden Mom Never Intended to Leave You

Your mom left you the house because she loved you, but she probably didn’t think about what that really means for your daily life:

The immediate costs hitting you:

- Utilities running in an empty house: $200-350/month

- Insurance and property taxes: $300-500/month

- Basic maintenance and security: $100-400/month

- Total: $600-1,250 every month the house sits empty

The decisions piling up:

- Do you winterize the pipes or keep heat running?

- What do you do with all her belongings?

- Should you update anything before selling?

- How do you handle repairs you discover?

- What if there are title or estate issues?

The emotional weight: Every time you drive by mom’s house or get another bill, you’re reminded of your loss. Instead of processing grief, you’re dealing with contractors and insurance adjusters.

Why Most Denver Families Sell Mom’s House (And Why It’s Okay)

Here’s something no one tells you: Most people sell their inherited family home within the first year. It doesn’t mean you loved your mom any less.

Sarah from Highlands Ranch sold her mother’s house three months after the funeral: “I thought keeping mom’s house would keep her memory alive. But every month of bills and repairs felt like a burden she never would have wanted me to carry. Selling it gave me peace to grieve properly and use the money for my kids’ college – something mom would have loved.”

The reality for most families:

- You already have your own house and don’t need two

- The inherited house doesn’t fit your current life

- Managing it from across town (or across the country) is exhausting

- The money could solve other problems or create opportunities

- Mom’s real legacy is the love and values she gave you, not the building

Your 4 Options for Mom’s House

Option 1: Quick Cash Sale (1-2 Weeks to Freedom)

Timeline: 7-14 days to close and move on

Best for: Families who want to focus on grieving, not property management

What you get: Fair cash offer, complete peace of mind

This is the path most grieving families choose because it removes all the burden immediately.

How it works with SellFastDenver.com:

- You call Scott at 719-888-9962 or visit the website

- Quick evaluation of mom’s house (you don’t need to clean or repair anything)

- Fair cash offer within 24 hours

- Scott’s team handles all paperwork, title issues, estate complications

- Close in 7-14 days at a Denver area title company

- Walk away with cash and closure

Why Denver families love this option: “Scott understood we were grieving and made everything simple. We didn’t have to deal with repairs, showings, or any stress. Just signed papers and got a fair price for mom’s house. We could focus on healing instead of being landlords.” – The Johnson Family, Westminster

Option 2: Creative Financing Solutions (2-3 Weeks)

Timeline: 14-21 days

Good for: Families who want maximum money but can handle some complexity

What you get: Full market value through payment plans

Instead of one lump sum, you carry financing for a qualified buyer who takes over the property immediately.

Example: Mom’s house worth $350k

- Buyer puts $50k down (cash to you now)

- You carry $300k in financing at 6% interest

- Receive $1,800/month for 20 years

- Buyer handles all maintenance, taxes, repairs

The upside: More total money over time The consideration: Ongoing paperwork and payments to track

Option 3: Traditional Listing (2-6 Months)

Timeline: 60-180 days if everything goes smoothly

Challenges: High stress during grief, many decisions required

Potential return: Highest price, but after repairs and realtor fees

This means cleaning out mom’s belongings, making repairs, staging the house, managing showings, and dealing with buyer financing that might fall through.

Reality check: Most grieving families who start this route end up switching to a cash buyer after 2-3 months because it’s too overwhelming during an already difficult time.

Option 4: Keep Mom’s House

Emotional appeal: High – it’s mom’s house

Practical reality: Usually becomes a burden

Unless you plan to move into mom’s house or become a landlord, keeping it typically creates ongoing stress and expense that interferes with your grieving process.

Why Denver Families Choose SellFastDenver.com

Scott and his team understand that inherited houses come with grief, not just profit motives. They’ve helped hundreds of Denver area families handle inherited properties with compassion and professionalism.

What makes them different:

Local expertise: They know Westminster, Lakewood, Littleton, Englewood, Colorado Springs, and every Front Range neighborhood. No out-of-state investors who don’t understand Colorado markets.

Grief-sensitive approach: They’ve worked with countless families dealing with loss. No pressure, no rushing, just clear options and honest guidance.

Complete service: They handle title issues, estate complications, property cleanup, repairs – everything that would normally fall on you during an already difficult time.

Fair pricing: Their offers reflect current Denver market conditions. They make money by solving problems, not by taking advantage of grieving families.

Quick timeline: Most families close within 10 days and can focus on healing instead of property management.

The Emotional Benefits of Selling Mom’s House Fast

Beyond the financial relief, selling quickly often provides emotional benefits:

Closure: You can properly grieve without constant reminders and decisions Relief: No more bills, repairs, or property management stress Freedom: Use the money for things that honor mom’s memory – kids’ education, family trips, paying off debt Peace: Know that mom would want you focused on your family and future, not maintaining an empty house

Tom from Colorado Springs: “I kept mom’s house for 8 months, thinking I was honoring her memory. But every leaky faucet and insurance bill felt like stress she never would have wanted me to have. Selling to SellFastDenver.com let me focus on what mom really left me – her love and wisdom. The money helped my daughter with college, which would have made mom so happy.”

What to Expect Working with SellFastDenver.com

Your first call: Scott listens to your situation without pressure. He understands this isn’t just a business transaction – it’s about your family and your grief.

Property evaluation: Quick, respectful assessment. You don’t need to clean, repair, or stage anything. They buy houses in any condition.

Fair offer: Based on current Denver market conditions and the house’s actual condition. No games, no last-minute changes.

Simple paperwork: They handle estate requirements, title issues, and all legal complications. You just sign where needed.

Fast closing: Usually 7-14 days at a reputable Denver area title company. You get cash and peace of mind.

Ongoing support: They answer questions even after closing because they understand this is about more than just a property transaction.

Taking the First Step Forward

Mom gave you this house because she loved you, but she would want it to help your life, not complicate it. Most Denver families find that selling quickly gives them the freedom to grieve properly and use mom’s gift in ways that truly honor her memory.

You don’t have to figure this out alone. Scott and his team at SellFastDenver.com have guided hundreds of Front Range families through this exact situation with compassion, fairness, and complete professional service.

The hardest part is often just making the first call. Once you do, you’ll have a clear path forward and support from people who understand what you’re going through.

Mom’s greatest gift wasn’t the house itself – it was her love and the opportunity to build your own future. Let SellFastDenver.com help you transform this burden back into the blessing she intended it to be.

www.SellFastDenver.com delivers cash offers in 24 hours and closes in 7 days—far faster than traditional MLS listings, which often take 45 to 90 days to finalize. To learn more or request a free, no-obligation cash offer, visit https://SellFastDenver.com or call Scott at: 719-888-9962